Active Management and the Predictability of Markets Redux: Robert Shiller

- Peter Elston

- Sep 1, 2019

- 5 min read

Updated: May 17, 2022

This is the second in a series of four posts dedicated to active management, focussing on some of the key figures involved in the study of market predictabilities. Having last month written about the “father of modern finance”, Eugene Fama, this month I take a look at Yale economist, Robert Shiller.

"That markets are neither rational nor efficient now seems obvious"

Shiller was co-winner of the 2013 Economics Nobel Prize alongside Eugene Fama. To many, it seemed a mistake - or at least a contradiction - that these two should share the prize. Fama is best known for the finding that markets were efficient or, rather, that they were efficient once trading costs were accounted for. Shiller on the other hand found the opposite, namely that there existed market mis-pricings that were big enough to profit from net of costs.

Although Fama is known for his early work which labelled him as a believer in efficient markets, his later research uncovered patterns and mis-pricings that he nowadays seeks to profit from through his work with Dimensional Advisors. These patterns, among others, related to the size and valuation of stocks (he found that small caps tend to outperform large caps and high book-to-price stocks outperform low book-to-price ones).

In a 1981 paper, Shiller showed that stock prices move much more than they should if they were purely a function of subsequent changes in dividends, also known as the “efficient markets model”. Later, in 1984, he showed that there was a positive correlation between the current dividend yield and subsequent returns. In other words, when the dividend yield was high, the subsequent one year price movement was higher than normal, contrary to the efficient markets model which implied that “a high current yield should correspond to an expected capital loss to offset the current yield”.

Fama, in collaboration with Kenneth French, showed in a 1988 paper that dividend yields had even greater predictive power over longer time frames. The two found that while dividend yields typically explained less than 5% of the monthly or quarterly stock market returns, they often explained more than 25% of 2- to 4-year returns.

Shiller’s work on asset prices, and in particular his 1984 paper, “Stock Prices and Social Dynamics”, paved the way for the emergence of the field of behavioural finance. Although the term “animal spirits” was coined by John Maynard Keynes in his 1936 publication, “The General Theory of Employment, Interest and Money”, it was popularised only later by Shiller himself and a colleague George Akerlof in their 2009 book “Animal Spirits: How Human Psychology Drives the Economy, and Why It Matters for Global Capitalism”.

That markets are neither rational nor efficient now seems obvious though it took several decades to challenge the widely accepted principle that human beings, the agents of markets and economic systems, make rational decisions. Charlie Munger, Warren Buffett’s business partner, famously remarked “If it isn’t behavioural, what the hell is it?” though this was in reference to economics rather than financial markets.

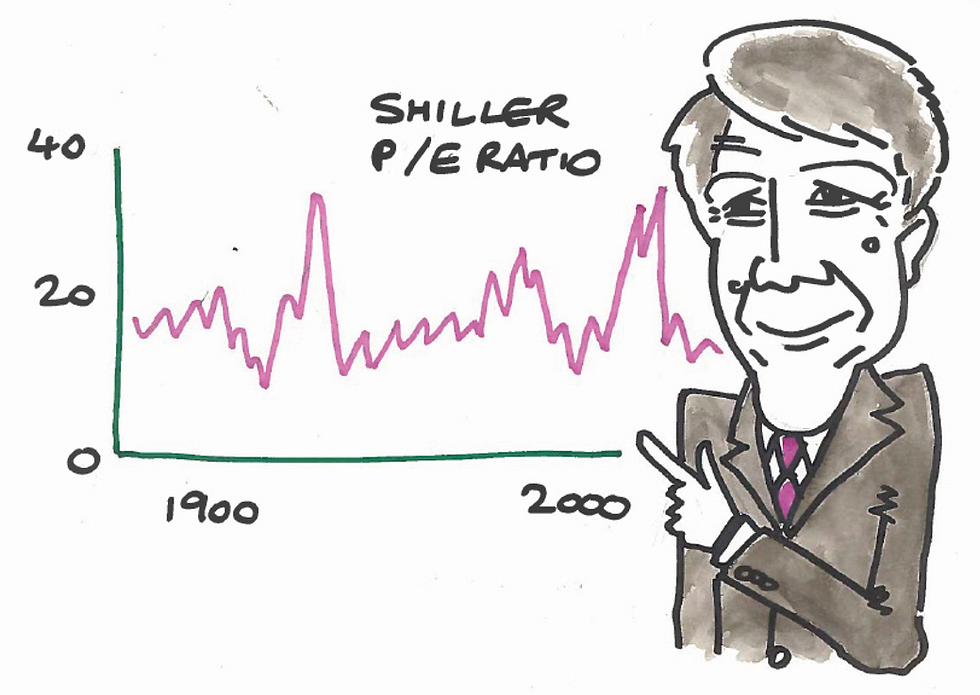

Although not mentioned in the paper that provided the background to the Nobel 2013 award, Shiller is also now associated with another predictive indicator, the cyclically adjusted price-to-earnings-ratio (CAPE), also dubbed “the Shiller PE”. CAPE is calculated by dividing the current price by the average 10 year real earnings and is based on the work of Benjamin Graham and David Dodd.

In their 1934 classic, Security Analysis, Graham and Dodd suggested that more meaning could be garnered by using smoothed earnings rather than current earnings. When earnings were depressed, they argued, the market would anticipate them recovering and thus trade on an ‘artificially’ higher multiple. Taking the ten-year average meant that one should always or at least most of the time be including both a peak and a trough in earnings and thus allow comparisons between current CAPE and historic CAPEs to be made on a like-for-like basis.

There is also a reasonably strong inverse relationship between the CAPE and the inflation rate (other than when inflation is negative) so it is possible that if central banks are able to prevent the world from slipping close to or into deflation and weak aggregate demand prevents inflation from accelerating sharply, a higher CAPE would be justified.

Prof Jeremy Siegel, famous for his 1994 classic Stocks for the Long Run, is another fan of the ratio but has argued that the data on which it is based can be unreliable. In 2013, he suggested that adding back write-downs incurred by financial firms in 2008 and 2009 would have raised ten year average earnings. This would have lowered the CAPE to a level which suggested the US market was still cheap. In view of the performance of US equities since 2013, his analysis appears astute.

John Hussman of US firm Hussman Funds was another who argued that earnings have been distorted (downwards) by accounting standards such as FASB 142, introduced in 2001. This standard “offers guidelines on adjusting the value of intangible assets, instead of keeping those investments on the books at cost and gradually amortizing the value over time. It’s argued that during the last couple of recessions this new accounting rule has caused companies to aggressively write down the value of their intangible assets, impacting earnings, therefore pushing profits lower, and biasing P/E ratios (like the CAPE) higher.”

What are Shiller P/Es and dividend yields currently telling us about current prospects for equity markets? In the case of the S&P 500 Index, the Shiller PE is currently 30.7 times. This is higher than 92% of monthly readings since 2005 and 96% of readings since 1871. As for dividend yields, the current yield on the S&P 500 Index is 1.9%, lower than 80% of monthly readings since 2005 and 77% of those since 1970. The US equity market and those elsewhere may very well go higher and become more expensive in the short term but, statistically, they will almost certainly be lower than current levels at some point in the future. The petrol gauge light is on. The question is, how much further do you want to carry on driving?

Published in Investment Letter, September 2019

The views expressed in this communication are those of Peter Elston at the time of writing and are subject to change without notice. They do not constitute investment advice and whilst all reasonable efforts have been used to ensure the accuracy of the information contained in this communication, the reliability, completeness or accuracy of the content cannot be guaranteed. This communication provides information for professional use only and should not be relied upon by retail investors as the sole basis for investment.

Comments